Fed Speak- The FOMC meeting for December was held from December 17-18, 2024, during which the Fed, as expected, lowered the federal funds target range by 25 bps to 4.25% to 4.50%. The FOMC statement issued on December 18th noted that economic activity continued to expand at a solid pace. Labor market conditions have been easing, with the unemployment rate ticking up slightly, though it remains low. Inflation has made progress toward the Committee’s 2.00% objective, but it remains somewhat elevated.

- Regarding future movements in the Fed’s target range, the Committee reiterated its commitment to carefully assessing incoming data and balancing the risks on both sides of its dual mandate (full employment and price stability). With regard to balance sheet policy, the Committee will continue to reduce its holdings of Treasury securities, agency debt, and agency mortgage-backed securities. The Committee remains committed to returning inflation to its 2% objective.

- Powell’s speeches have, of late, tended to move markets. Whether this is necessarily healthy for markets is up for debate. As markets are forward looking, much depends on any indications of future policy rate paths and balance sheet policy. Powell highlighted that job gains have slowed from earlier this year, averaging 173,000 per month over the last three months. Nominal wage growth has eased over the past year, the job-to-worker gap has narrowed, and a broad set of indicators suggests that labor conditions are now less tight than 2019 levels. Powell therefore concludes that the labor market is not a source of inflationary pressure.

- The decision to lower the target range for the federal funds rate by another quarter point represents a full-point reduction from peak restrictive policy. Powell notes that they have been moving policy toward a more neutral stance to maintain the strength of the economy and the labor market while making further progress on inflation. The Committee understands that lowering the rate too quickly may hinder progress on inflation, while doing so too slowly could risk unduly weakening economic activity and employment.

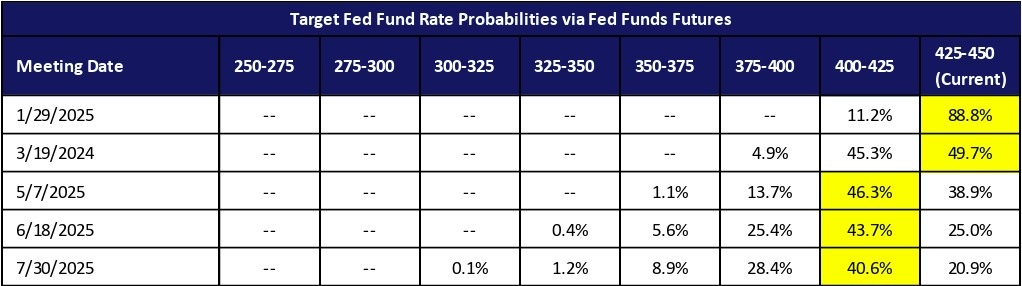

- In the Q&A that followed, questions surrounding the “extent and timing” language in the Committee’s statement prompted additional guidance from Chair Powell that supported a stall in the degree of rate cuts going forward in 2025. Powell noted that GDP growth has remained very strong and that going forward, while inflation remains a bit sticky, the Committee plans to wait and assess data as it comes in. The trajectory of rate cuts for 2025 was reduced to two from four.

- The rate cut in December was not unanimous. Cleveland Fed President Beth Hammack cast a dissenting vote. The reluctance of a significant minority at the meeting to move rates was driven by an upward revision for GDP growth and inflation forecasts for 2025, as well as a downward revision of unemployment forecasts for 2025. With that backdrop, Hammack and three other participants, who could not vote, were opposed to the move.

*As of 12/31/2024 Macro Environment- The employment landscape improved to 227,000 in November, up from an upwardly revised 36,000 in October, which had been impacted by disruptions from hurricanes and strikes at Boeing. This reading exceeded forecasts of 200,000. Employment increased in health care, leisure and hospitality, government, and social assistance. Employment also rose in transportation equipment manufacturing, reflecting the return of workers who had been on strike. Retail trade lost 28,000 jobs in November, with general merchandise retailers accounting for -15,000 of the net losses in the sector. The unemployment rate remained unchanged at 4.2%. 425-450 (Current) 88.8% 49.7% 38.9% 25.0% 20.9%

- The University of Michigan’s Consumer Sentiment index rose to 74.0 in November, up from 71.8, marking the highest level since April 2024. While this increase signals optimism, it was somewhat muted by heightened inflation expectations. A surge in buying of durable goods — items with a useful life of three years or more (such as cars, electronics, furniture)—helped lift the index, likely driven by increased caution regarding future prices of these goods. Notably, the survey results revealed a divide along political lines, with Democrats largely expecting inflation pressures due to President-elect Trump’s tariff proposals, while Republicans and Independents believed price pressure would continue to ease.

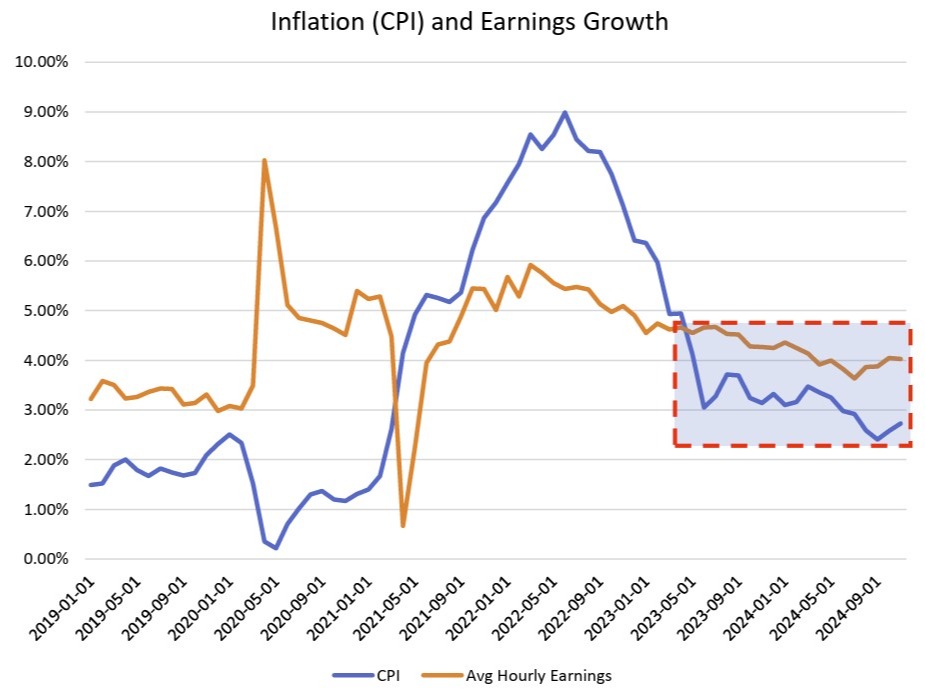

- The inflation picture remained stable, as noted by Powell in his FOMC meeting address. November readings for CPI and Core CPI both rose 0.3% month over month, or 2.7% and 3.3%, respectively, year over year. Over the twelve months ending November 2024, one of the main drivers of disinflation in the headline number was a reduction in energy commodities, fuel, and gasoline. Fuel oil prices were down 19.5%, and gas was down 8.1%. Core CPI, which excludes volatile food and energy prices, was driven by persistently high shelter costs and transportation services, which were up 4.6% and 7.1%, respectively, year over year. Looking ahead to 2025, there is uncertainty regarding whether we will see a resurgence in inflation, as oil prices finished the year at ~$75 per barrel. Another consideration will be future tax and tariff policies and their potential impacts on inflation.

- Wage growth, as measured by average hourly earnings for all nonfarm payroll employees, rose 0.4% in November, or 4.0% year over year, to $35.61 per hour. Wage growth has remained consistently above inflation since H1 2023, which is expected to contribute to continued consumer strength in 2025.

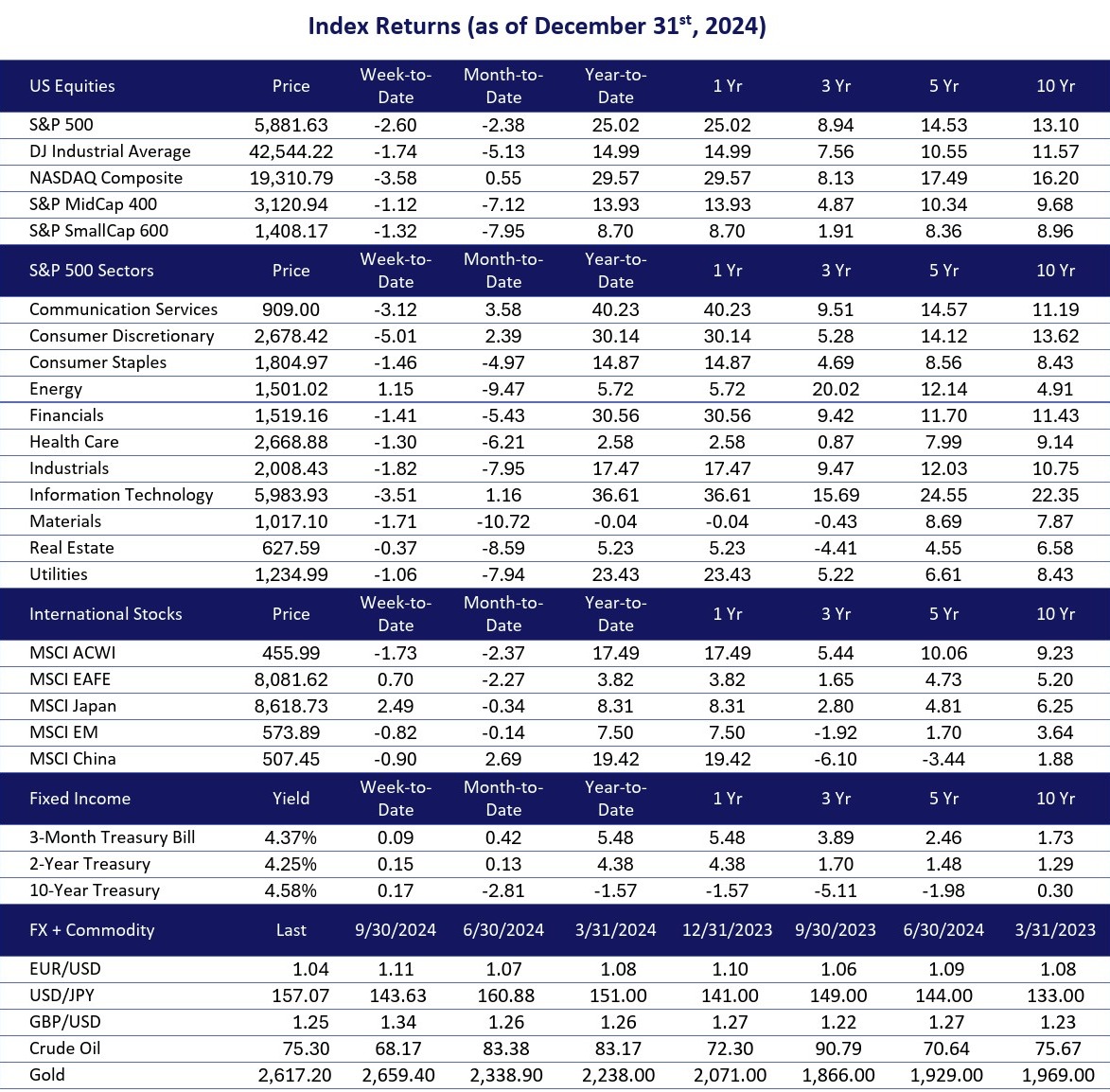

Market Performance and OutlookDecember marked a lackluster end to an otherwise very strong year for US equities. For the month, only the NASDAQ eked out a small gain of 0.55%, while the S&P 500 and DJA fell by 2.38% and 5.13% respectively. Small and mid-caps also suffered, with the S&P Midcap 400 and Small Cap 600 each falling over 7%. From a sector perspective, information technology stocks finished the month with a 1.16% gain, while the top performers were communication services and consumer discretionary, gaining 2.39% and 3.58%, respectively. The rest of the sectors were in the red in December, all posting losses at or below 5%, led by major selloffs in materials, energy, real estate, and industrials. For the year ending 2024, communication services were the winning sector, gaining over 40%, driven by the inclusion of several of the Mag 7 names, like Alphabet, Netflix, and Meta, which surged on AI optimism. Closely behind were technology services, which rose by 36%. From a factor perspective, growth, momentum, and large cap stocks had an exceptional year, gaining 35.8%, 31.99%, and 27.94%, respectively. High dividend yielding stocks, small caps, and value stocks lagged in 2024. 2024 was a great year for US stocks relative to developed international. The MSCI USA index returned 24.5%, while the MSCI EAFE returned only 3.82%. The yield curve continued to steepen in December, with the long end of the curve rising notably in Q4 despite the Fed’s cuts to the short end, primarily driven by heightened inflation expectations for 2025 and mounting fiscal pressures. The US fiscal situation is a headwind. The Fed has stated it plans to continue reducing its balance sheet holdings, leaving institutional and other sovereign investors to take down the auctions. This week’s auctions include $58 billion in 3-year notes, $39 billion in 10-year notes, and $22 billion in 30-year bonds. As the front end of the curve falls with Fed rate policy, bonds now appear more attractive than cash. Looking ahead to 2025, there is reason to believe that markets can build on some of the successes of 2024. Valuations have expanded, particularly in large cap technology and communications sectors, but growth tailwinds set the stage for continued earnings strength, which can support those valuations. The consumer remains relatively strong, having managed to stretch their budgets and consume 3% more year over year, despite higher prices. Wage growth is now higher than inflation, which is important as consumer spending accounts for roughly 70% of GDP. The Fed has stated that they will likely slow the path of interest rate cuts, much of which has already been priced into the late December selloff in interest rate sensitive sectors. While it is important to avoid letting inflation run away again, the federal funds rate appears to be reasonably restrictive relative to inflation, providing the Fed some runway and room to cut rates as needed. Importantly, there don’t seem to be signs of a looming recession, despite one of the longest yield curve inversions in history, which ended in H1 2024. There is an opportunity for some of the underperforming sectors to catch up to the strong performance of growth stocks in 2025. Small- and mid-caps, value stocks, and dividend paying stocks lagged in 2024. A catalyst is needed to unlock this value, but pricing is favorable, and these sectors derive a larger portion of their revenues from the US, which we believe will retain its relative strength within the global economy.

Source: MorningstarDirect. Returns greater than one year are annualized. Please note the fixed income datapoints are returns and not changes to the yield. U.S. Equity section contains price return price levels and total return calculations.

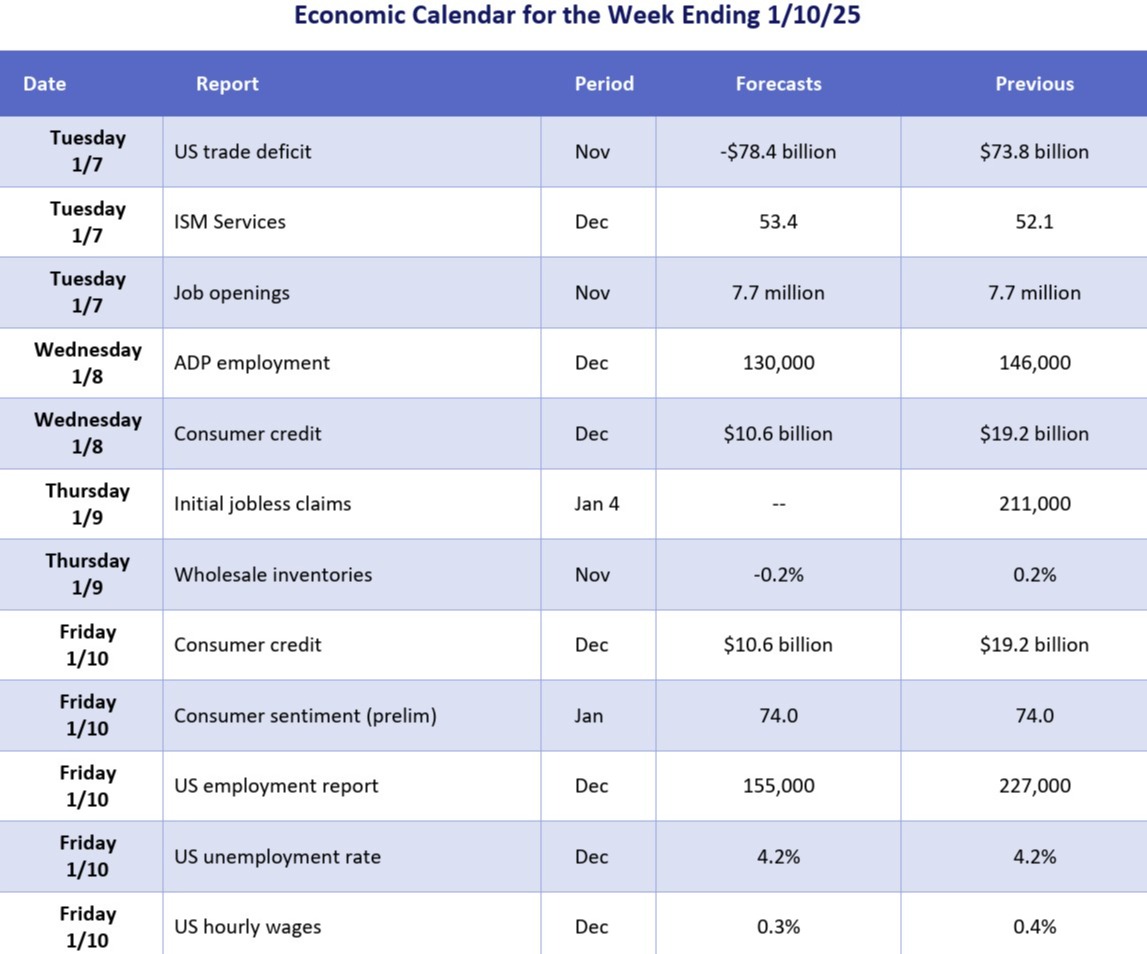

Source: U.S. Economic Calendar - MarketWatch. |